How Tax Works

Join host Matthew Foreman, Co-Chair of Falcon Rappaport & Berkman’s Taxation Practice Group, on "How Tax Works," a podcast attempting to unravel the complexities of the tax law, caselaw, and guidance. In each episode, Matt simplifies this intricate labyrinth of tax law, breaking down complex concepts into easily digestible explanations. From understanding how tax considerations impact decision-making processes to dissecting the structural nuances of businesses, Matt sheds light on the oft-misunderstood world of taxation.

Through real-life examples, and practical advice, "How Tax Works" seeks to equip listeners with the knowledge they need to navigate the intricacies of taxation confidently. Whether you're an accountant, lawyer, business owner, or simply someone who wants to understand how tax shapes business and financial decisions, How Tax Works is your go-to resource for demystifying the complex that is taxation in America.

This podcast may be considered attorney advertising. This podcast is not presented for purposes of legal advice or for providing a legal opinion. Before any of the presenting attorneys can provide legal advice to any person or entity, and before an attorney-client relationship is formed, that attorney must have a signed fee agreement with a client setting forth the firm’s scope of representation and the fees that will be charged.

This Podcast is Hosted by:

Falcon Rappaport & Berkman LLP

1185 Avenue of the Americas, Suite 1415

New York, NY 10036

(212) 203-3255

info@frblaw.com

How Tax Works

Entity Selection

Use Left/Right to seek, Home/End to jump to start or end. Hold shift to jump forward or backward.

Welcome to the first episode of How Tax Works. Host Matt Foreman discusses what is likely the most important decision that a business owner can make: Entity Selection. Matt will discuss many of the tax and non-tax factors, ways to weight those factors, and the tax effects of each type of entity. This episode is for business owners, attorneys, accountants, and their advisors, as well as anyone who has ever wondered whether they should make a S election.

Attachment Here

{kind=link}

How Tax Works, hosted by Falcon Rappaport & Berkman LLP Partner Matthew E. Foreman, Esq., LL.M., delves into the intricacies of taxation, breaking down complex concepts for a clearer understanding of how tax laws impact your financial decisions.

Follow us on Bluesky:

@howtaxworks.bsky.social

This podcast may be considered attorney advertising. This podcast is not presented for purposes of legal advice or for providing a legal opinion. Before any of the presenting attorneys can provide legal advice to any person or entity, and before an attorney-client relationship is formed, that attorney must have a signed fee agreement with a client setting forth the firm’s scope of representation and the fees that will be charged.

This Podcast is Hosted by:

Falcon Rappaport & Berkman LLP

1185 Avenue of the Americas, Suite 1415

New York, NY 10036

(212) 203 -3255

info@frblaw.com

Matt Foreman [00:00:08]:

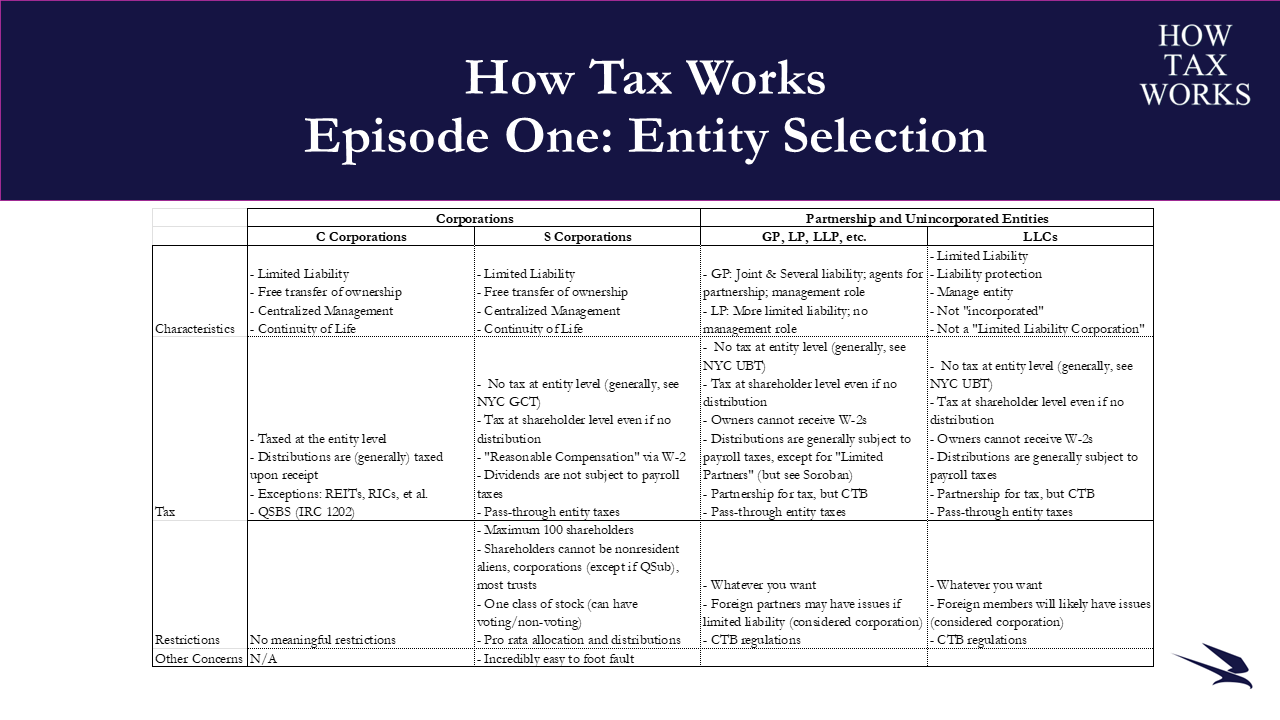

Welcome to the first episode of how Tax Works. I'm Matt Foreman. In this episode, I will discuss enity selection, which is perhaps the most important decision a business owner will make. How tax works is meant for informational and entertainment purposes only. This may be attorney advertising, and it is not legal advice. Please hire your own attorney. How tax works is intended to help listeners navigate the intricacies and complexities of tax law, regulations, case law, and guidance to demystify how taxes shape business and financial decisions that we all make. On the page for this podcast is a handout, which I'm going to reference repeatedly as I go through this.

Matt Foreman [00:00:47]:

It's intended to facilitate my discussion. It is nowhere near every single consideration, but I think it does a fairly good job. I admit I'm biased of going over a lot of the main points that I'm going to cover and some of the most important ones. Generally speaking, when you're deciding what entity to be, there are two countervailing considerations. There are legal considerations, often referred to as corporate, and there's tax considerations. From a corporate perspective, you want as much protection as possible. But from a tax perspective, you actually want, instead of worrying about how much protection you have, you actually want to lower your taxes, right? That's the standard complaint. And so as a result, you know, different entities and things have changed over time and the laws changed.

Matt Foreman [00:01:32]:

Try to marry those two concepts. They don't always work together, and they're often, as I said earlier, countervailing. One goes up, one's better, one's worse, and you try to get to the right area, the right mix between. Basically, I'm going to go from the top left to the bottom right, except for when I talk about it. So from the first start, you know, first beginning, we're going to talk about C corporations, right. Various characteristics of C corporations, right. Corporations generally, CN's, from a non tax perspective, are really the exact same thing. Limited liability, free transferability of ownership, centralized management, continuity of life.

Matt Foreman [00:02:08]:

The continuity of life is really interesting, so I'll kind of go bottom up here, but continuity of life, initially, a lot of entities had to be basically in the beginning, renewed every year, which sounds very weird to anyone today, right. Most entities are forever. So that obviously went away the way of the dodo, unfortunately. And so it has that corporations have central management, right? They have boards, they have CEO's, things like that. You can transfer shares, own, you know, anyone can own them. And there's generally limited liability. Some states, and depending on the entity, the federal government may limit that liability of specific instances, but that all depends how things go. Then there are partnerships and unincorporated entities.

Matt Foreman [00:02:51]:

Unincorporated entities that fit into this are really just any business that does not have an entity itself. You know, sole proprietorships are the main thing, but really anything that's what's called unincorporated really means. Anything that's any sort of partnership or a limited liability company, anything that's not a corporation for the GP, LP, LLP, etcetera, you know, general partnerships tend not to have entities, or you can form a general partnership, joint and several liability. Everyone's liable for everything. The owners and the people operated are really agents for the partnership and have a management role for limited partnerships, limited liability partnerships, things like that. It limits liability. More significantly. There's no direct management role except for, you know, from the partner side, except for what they're allowed to do as basically officers of the partnership.

Matt Foreman [00:03:44]:

The LLC, of course, that's the unincorporated entity that most entities these days are right, has limited liability. Limited protection. I'm sorry, liability protection. You know, they're going to be managed by a board, by the people who run it, by the managers. There's a lot of different terms. They're not incorporated per se, and they're not, you know, I hear this from time to time, what's called a limited liability corporation that does not exist in any meaningful sense. Corporations are corporations. Limited liability companies are a separate thing.

Matt Foreman [00:04:13]:

They're a product. They've only been around for 35, 40 years, which in the scheme of things is pretty short, believe it or not. And they're really going to talk about, when you think about llcs is they have a lot of the protections from a liability perspective that corporations have, but they have passed through taxation. And I'm skipping ahead a moment here, but I think it's really important to note that they're sort of a hybrid right, between corporations and partnerships. The biggest, you know, thing, the biggest thing for llcs was there was a whole question, you know, what are llcs from a tax perspective? Prior to what's called the check the box regulations, there was a four factor test that determined what they were, and the IR's came out and determined that llcs are partnerships and that really allowed llcs to just explode. After that, every state made sure they had them. They became by far the most formed entity except for certain circumstances where you want something else. Now go through the tax considerations.

Matt Foreman [00:05:13]:

This is a tax podcast, after all. So I think it's important to discuss. I'm going to go c corporations, then into partnerships, and then back to s corporations. I think that's the most logical order to do it. C. Corporations. Right. Tax at the entity level, there is a 21% tax.

Matt Foreman [00:05:31]:

It's a flat tax. So you make $100, you pay $21 a tax. That's it. Plus state taxes. They generally are between four, six, 8% dependent upon the state, and that's taxed at the end of the level. No matter what, distributions are generally taxed upon receipt. There's exceptions to that, and there is no deduction, again, generally, for any distribution. So you pay the 21% tax, and any distributions are going to be after that.

Matt Foreman [00:05:58]:

The taxes on that are generally. It's generally taxed even though it's an ordinary dividend. They're taxed at the capital gains rate. So that's generally 23.8% is the highest rate. It's graduated. So it depends on your income level, plus whatever the state has. So that can be anywhere from zero. For someone who lives in Nevada or, I think New Jersey has the highest, but I'm not sure, you know, New Jersey, New York, California, there's a few others that kind of stick in there.

Matt Foreman [00:06:24]:

The main exceptions to this are reits, Rics, and a few others. They exist for very, very, very specific purposes, right. Investment companies, real estate, etcetera. And they often require other certifications or licenses to exist. So unless you're doing what they are, they don't really make sense. And the truth is, a lot of times those entities just fall into llcs. They become pass throughs, otherwise, so there's no really reason to do it. A lot of those entities have required distributions, and they're actually taxed at the entity level, generally speaking.

Matt Foreman [00:06:55]:

And then they get a deduction for any dividends they pay. So it's an exception to the general c corporation rule. But as I said, they have other requirements that are really important to make sure to follow. So if you don't want to be a reit or a ric, don't. There's other, you know, similarly tax efficient ways to do it. You'll notice that, you know, the two columns for all the partnerships and unincorporated entities are pretty similar. Kind of talk about them in parallel. But basically, there's no tax at the entity level.

Matt Foreman [00:07:28]:

That's in general, there are exceptions to that. A number of states cities have entity level taxes, generally referred to as a UBT unincorporated business tax. Again, unincorporation, unincorporated entity, anything other than a corporation. New York City's is probably the most famous 4%. A number of other states have it. You know, Connecticut, New Hampshire, a few others have implemented it. I'll talk about pass throughout the taxes in a moment. There is, you know, basically, even if there is no distribution, if the owners do not get anything, right, there is a tax at, I use the word shareholder, but it's really member or partner level people who own part of the entity.

Matt Foreman [00:08:10]:

And I think that's important. People always say, look, I didn't get any money, I didn't make any money. How can I owe taxes? And the answer is, the trade off is if you go back to c corporations, 21 plus state and then 23.8 plus state, much higher tax rates. All the partnerships are basically 37%, it's graduated plus the state rate. So what happens essentially is in exchange for lower taxation, you have to deal with the fact that you are taxed even if you don't distribute, you know, all the money or even any of the money, right. I always point out, and I think this is a really important point, that if you're never going to pay a distribution, right, or anything like that, you want to keep maximally reinvesting, you want to lower your tax rate. It's actually lower to be a C corporation because it's 21% rate plus state, as opposed to 37.37% plus state for any partnerships, right. And s corporations would be the same.

Matt Foreman [00:09:10]:

We'll get there in a second. So for some businesses, being a C corporation can actually lower your taxes. There's other reasons, other considerations. Any partnership or llcs, right. Owners cannot receive w two s and the distributions are generally subject to payroll taxes. Except for limited partners, payroll taxes are 15.3%, up to a little less than $170,000. And then at $170,000, what happens is only the employer side pays 7.65. So basically half, which of course is deductible.

Matt Foreman [00:09:44]:

The rate isn't really 15.3 because it's deductible on the employer side. So the rate a little bit lower than that, usually somewhere around eleven or twelve, it ends up with. The effective rate is, even if you're self employed, the limited partner exception, which exists for LP's only, is the basic premise is that a limited partner in a limited partnership does not have to pay payroll taxes. Right. It's just how it works. There's an exception in the rule. There is a recent case, Sorbonne Capital Partners. It's a New York City based fund.

Matt Foreman [00:10:20]:

I think they're technically venture capital or private equity. I never really remember. And basically what they had was a number of partners in that operated the business and their investments, their actual dollar investments, were as limited partners. What the tax court said was that simply having the name you're being a limited partner did not mean you were actually a limited partner for tax purposes. So even though you're called a limited partner, if you're active in the business, you may still be subject to payroll taxes, llcs, everyone's subject to payroll taxes. So that's not really an issue, as I say. Right, partnership for tax, but just CTP, check the box. The US is really interesting, one of the only countries that has anything like this.

Matt Foreman [00:11:06]:

There's a couple countries that have elective regimes for a couple entities, but the US really allows you to elect, and I'll get this into s corporations, but basically each entity type, Inc. Corporation, LLC, et cetera, et cetera, has a default tax type, right. Disregarded entity, partnership corporation, what have you. And then you can usually check the box, depending on your owners, the type of entity, and a few other factors. For example, you can be an LLC and check the box and be an S corporation or a C corporation. You can be a corporation, check the box, be an S corporation, you can be a trust and check the boxes of SC corporation and so on and so forth. There are tax reasons for doing it. There are tax reasons for not doing it.

Matt Foreman [00:11:49]:

And I really, really cannot stress this enough, you know, talk to a tax advisor and think about the consequences because it's really important. Pass through entity taxes. It's a bit of a misnomer. What it actually is is basically a workaround of a state and local tax cap, salt cap. And you know, New York has the bait. Excuse me, New York has the pizza, New Jersey has the bait. Every state has a fun little acronym, right? And what they are is basically it's elective and they shift the income tax incidence to the entity and then they provide a credit to the owner, right? And so what happens is you pay the tax, the entity level, it's deductible at the federal level. And then that basically means that the people who own businesses pay a lower effective tax rate because they're able to deduct their state and local taxes without a cap, right? The cap is really low, right? $10,000, I know it's indexed to inflation a little bit, but it's really pretty much $10,000 is fairly low for high income earners or anyone who lives in a high tax jurisdiction.

Matt Foreman [00:12:53]:

So it's really important from a constitutional perspective. I'm actually not sure in a law perspective that it's actually allowed. A lot of practitioners will admit with a bit of a cheeky grin that, you know, this is not allowed because it's technically an optional tax, even though you elect into it. Electing into a tax is not permitted to create a tax that is deductible right at the, at the entity level. But the IR's issued a notice saying it's okay. So even though that notice has no support, I'm not sure anyone really is going to challenge it because it would simply raise taxes on people. And generally speaking, that's not a situation where people challenge laws. They want to keep taxes low, right? There's a countervailing, again, countervailing goals with s corporations.

Matt Foreman [00:13:42]:

Very similar to the partnerships. Generally no tax at any level. But New York City, for example, ignores the s election entirely, not the state, just the city, and therefore imposes an 8.85% tax on New York City source income. For s corporations. It's tax, you know, similar to GPS LP's. All the partnerships, llcs, there's a tax at the shareholder level. Even if you don't distribute the income, you are required to pay reasonable compensation via w two to any s corporation shareholders that also work within the business, provide services, advice, what have you. Significant audit risk.

Matt Foreman [00:14:23]:

And the IR's has signaled that they are starting to audit that historically what people did was they decreased their reasonable compensation below frankly reasonable levels and as a result they maximized, you know the next point, right? Dividends are not subject to payroll taxes. So because dividends are not subject to payroll taxes, there is a benefit to not to paying yourself a lower reasonable compensation to minimize payroll taxes. So the IR's is saying, well, look, you know, Social Security not that well funded these days. So we need to make sure that it's done right, that reasonable compensation. There are audits, you know, recommend definitely something that people consider when choosing entity type. And also talk to your advisors making sure that's correct. You know, the dividends in addition to not being subject to payroll taxes, also the taxes on the dividends are eligible for ptets, right? Which I talked about with the partnerships and llcs. So as a result, you know, that those amounts can the taxes, the effective taxes are lower because you can deduct state taxes from your federal taxes.

Matt Foreman [00:15:25]:

So there is, you know, double benefit of decreasing the reasonable compensation. So that's a benefit, right. Then moving on back to C corporations restrictions. There's no meaningful restrictions on C corporation ownership, really. They are almost certainly the most easiest to own, most common to own, especially for foreigners, for reasons I'll get to in a moment. S corporations have by far the most restrictions on ownership, right. Maximum 100 shareholders used to be ten. People often say, you know, when will I have 100 shareholders? I have seen large medical practices, large law practices that have 100 shareholders and run into this issue.

Matt Foreman [00:16:05]:

There are ways to get around it. It is clunky and tough. Sometimes it requires tax to do, you know, recognizing tax and paying tax to do. The shareholders cannot be non resident aliens. So basically any individual or any foreign corporation, they can't be corporations in general. The exception to that is if a S corporation owns 100% of another S corporation, that's permitted. The main, the top corporations, just an S corporation, have to make an election. The lower tier corporations, what's called a Q sub qualified s corporation subsidiary, and that again, 100% owns.

Matt Foreman [00:16:42]:

So it's kind of pointless to have, you know, to stack them unless you have a business reason for doing it. From a tax perspective, doesn't help. Most trusts cannot be shareholders. Llcs can be shareholders and s corporations, but the LLC must be what's called a disregarded entity, which is just ignored for tax purposes. Partnerships definitely cannot. I don't recommend having llcs own, and the reason is it's very easy to mess that up. Estate planning can create a partner if you own it in a state that is not, you know, with a spouse. Right.

Matt Foreman [00:17:17]:

That can be a problem. That can be problematic as well. So there's a lot of reasons. You can only have one class of stock, so all the economic rights have to be equal with every share held by every shareholder. You can have voting, non voting, but it has to be binary. Cannot be double voting or half voting or whatever. The allocations and distributions must be pro rata, which means that if the S corporation makes $100, it has 100 shares, each share will get $1 allocated to it. If you make a distribution, each share will get 1% of whatever the distribution is.

Matt Foreman [00:17:48]:

Contrast that with any partnership. Right. Whatever you want really is for the entities. You know, you can do whatever you want. Anyone can own it. There's no issues. Foreign partners may have issues, and this is a really important one. I'm going to take a pause here to discuss this.

Matt Foreman [00:18:05]:

It's really important to note that foreign individuals, they can own partnerships. This is a situation where limited partnerships, general partnerships, are very, very common. Still, if foreigners own part of a us business that is not a c corporation, obviously can't hold ownership in an S corp. A lot of countries, basically every country views llcs as if they're c corporations, which creates an interesting mismatch where what happens is the foreign country views the tax that's paid by the owners of the LLC as if it's a corporate tax and can have a problem with the foreign tax credit, basically making taxes uncreditable, which when you distribute income back up to the foreign country, the foreign owner, it can create a level of double to true double taxation. So if you have foreign owners, we should talk, you know, talk to your tax advisor, make sure they have experience with cross border structuring and they can do it. Even Canada has this issue, right? Canada views llcs as if they're c corporations. So it has a problem. So it can really bump up the overall tax rate.

Matt Foreman [00:19:11]:

There's also what's called hybrid and reverse hybrid entities. This is what I was just talking about where one country views it as transparent, one country views it the other way. Right. Foreign LLCs are not viewed as if the same way as if it's a US LLC from the us perspective, most foreign llcs are viewed from the us perspective as if they're corporations. So you really have to watch out. The biggest benefit that the US has here is what's called the check the box regulation, CTB. And what that allows businesses to do is choose how they're taxed. You can have an LLC taxes, C corporation, you can have an LLC taxes and S corporation.

Matt Foreman [00:19:48]:

Llcs can be taxed as partnerships, things like that. So since it's largely elective, you can have, you can use an LLC to be held by foreign individuals, but you probably just want to use a corporation. What people do is they held by an LLC, they check the box. I've always found that was a little clunky. Why not just be a corporation? Why make extra work, right? Unless you're really just really excited to file extra forms to the IR's with a state. I never really understood that. But you can. As I note other concerns at the bottom, it is incredibly, incredibly, incredibly easy to foot fault with s corporations.

Matt Foreman [00:20:29]:

I've seen it many times where, you know, they make a loan to one partner, not the other, that may blow the s election. So you may be a C corporation. And I always say this is if you're an LLC and you make the s election, if you blow the s election, you don't go back to being taxed as a partnership. You go, you go to being taxed as a C corporation. And if there be returns, whole, whole thing. So if you're looking to sell your business, that's something a buyer is absolutely going to look at. If you're looking to get an investor, you know, it's really hard to get investors and s corporations, we do a lot of times when they're being sold or investments, what's called fre orgs, which basically allows you to be taxed as the partnership. So for a lot of times when I'm talking to clients, I often say, what are your goals for one year? For five years, and for 15 years, one year, they can usually explain five years, probably 15 years.

Matt Foreman [00:21:19]:

Who even knows? Who knew 15 years ago in 2009, how much the world had changed, would change by 2024? So I think it's really important to have that conversation, think about the long term and what you're trying to accomplish. So, you know, it's important. Like I said, comparing S corporations with partnerships, right. They're both pass throughs, whereas C corporations, right. I always say this. Look, pass throughs, if you're going to distribute all or the vast majority, even probably most of the income, two thirds or so, you're going to have lower overall taxes. But if you don't distribute, right, with a partnership or an S corporation, any sort of pass through, the taxes are actually going to be higher if you don't distribute, because you're going to have to come out of pocket for it if you're a corporation. Since the corporation is the one that actually pays the taxes, the taxes are lower overall on a year over year basis.

Matt Foreman [00:22:11]:

If you're not distributing, there's also a qualified small business stock, section 1202. Following along, you notice I skipped it. Section 1202 of the code is not a loophole. It is quirky. It has some very, very finicky rules, and it exists somewhat on an island because it really doesn't, this kind of exclusion does not exist anywhere else. So it's something that you really want to watch out for and think about when you're trying to, when you're trying to qualify. Basically, a business is a call, has qualified small business stock. If it is in certain business areas, it is much easier because this is how the code section works, to talk about the business types that do not qualify.

Matt Foreman [00:22:55]:

Right. First off, has to be an active bit trader business. So that's really important. Cannot be some sort of passive investment company. Generally speaking, it's a little more broad than this. But any service business, financial services, insurance, things like that, right? So lawyers, doctors were out. Financial services, real estate management, things like that, those are out. Those are not qualified.

Matt Foreman [00:23:16]:

But if you have a company that's doing software development, if you are a company that is buying and selling things online, right. Depending on what it is that may qualify. You have to hold the stock for five years. You have to get the stock from the company itself and initial issuance. There's other rules around whether there was a redemption of a large redemption they're worried about. Since you can't get qualified for the business stock by buying it from another shareholder, they don't want them to redeem that shareholder, then immediately resell or resell it, then redeem it. So there's rules around that. Also.

Matt Foreman [00:23:48]:

When you buy the stock, when you acquire it, and you don't have to just buy it, you can provide services and get equity in exchange. Right. Sweat equity works. The assets have to be less than 50 million. Right. And that's most businesses. But I always say that a lot of times this happens in conjunction with a raise. And people say, well, how much are the assets worth? And the answer is, well, how much does the capital raise say the assets are worth? If you're buying, they're selling 10% of the company for $5.5 million.

Matt Foreman [00:24:15]:

Well, that means the company's worth 55 million. Right. Post money. And that would mean that the stock you acquired is not worth qualified small business stock. I have seen people, instead of raising at 55 or something like that, raise it 49, nine, because they feel that it will be much, much easier to raise, and the dollar amount's not that different. Or other factors for substantial people are like, oh, I'll just be an LLC, and then right before I sell or five years before I sell, I'll become a C Corp. Right. Or be an LLC for a period.

Matt Foreman [00:24:45]:

No. Substantially all the time that the business operates, it must be a C Corp. Right? Substantially. All is not defined in this context. Generally, I want people over 80%. Some people say 90. I've seen people say as low as 60. I think that is extremely, extremely aggressive.

Matt Foreman [00:25:04]:

You really want to be a little conservative. If you're targeting QSBs, just start the business as a C corp. You know, that's it. And it's also important to note that there are a number of states that decouple from this, which means they don't follow qualified small business stock. New Jersey. Right. I'm in New York. Never miss an opportunity to make a joke about New Jersey.

Matt Foreman [00:25:23]:

New York follows. New Jersey doesn't. Right. So if you live in New Jersey, your taxes are higher. New Jersey will tax, federal government won't. Right. Live in New York. Right.

Matt Foreman [00:25:31]:

New York will not tax. If you qualify for small business stock, again, up to 10 million per shareholder, or it's also, ten times your initial investment. So if you invested, you know, 10 million in a company, right, then you have a hundred. You have up to $100 million in qualified small business stock. Ten times ten equals 100. And I can do that math. But if you invest, you know, $200,000, then you have 10 million. It's basically the larger of ten times your investment, or $10 million for the vast majority of shareholders, it's $10 million.

Matt Foreman [00:26:02]:

There's other really kind of quirky rules around putting a partnership on top, an LLC on top. Afterward, there's rules around splitting it. There was an article in the Times maybe two years ago at this point about using trust to split it to maximize qualified small business stock. If you want to do that, talk to someone who has experience with it. And I think it's really important. And then I think the last thing major point I'm going to bring up is state and local tax considerations. I discussed the GCT and the UBT at the high level, but I want to dig into it a little more because I think it's really important to think about it. And this is a situation where if you ignore state and local tax, that that's at your own peril.

Matt Foreman [00:26:42]:

It can really create issues. As I said earlier, New York City ignores s elections, and it does that by imposing the general corporation tax GCT on S corporations. Conversely, every other kind of partnership, any partnership, disregarded entities, sole proprietorships have what's called, are subject to the unincorporated business tax, or UBT, whereas the GCT is 8.85% from dollar one. You make $100, you pay $8.85 a tax, you're done with the UBT. The first $85,000 of income is not subject to tax. And then there's this kind of weird crediting mechanism. And what happens is as your income level goes up and this is on a per owner basis up to 135,000, your rate slowly ticks up. And then income, once you hit 135,000, it's taxed flat at 4%.

Matt Foreman [00:27:35]:

So there's also a credit that you can get if you're a resident of the city or the state. And there's different rules on that which I'm not going to go into. I'm basically going to ignore them because they're just more complex and they're very formulaic. The rate for a lot of New York City residents is actually 3.08%, but I just say it's 4%. I've often found that if you tell a client that the rate's four, and then it's 3.08. They don't really complain. If you tell them it's 3.08 and the rate's four, they're going to complain. Right.

Matt Foreman [00:28:02]:

So, so, so, you know, promise low, deliver high. Right. And that's the premise. A lot of people, they, you know, you get these small businesses in New York City and they become s corporations, and as a result, they actually pay more taxes. Right. And that's not helpful. You know, that's not good. That's not what the code wants.

Matt Foreman [00:28:17]:

They want you to choose the right thing. So I often ask people, you know, are you going to operate in New York City? Are you going to have clients in New York City? Right. Most jurisdictions at this point are market based sourcing. So even if you're not operating in the city, but you have a lot of clients in the city, you're coming into the city a bunch, etcetera, that can really trigger that. So you really want to watch out for that. And as I said earlier, New York City is not the only city that has this New York City. You know, there's states that have taxes on pass through businesses, and I think it's important to really watch out if you don't pay attention, you know, as the doctor will say. Right.

Matt Foreman [00:28:48]:

Pay attention to your salt. You got to pay attention to your salt. That's it. I hope you learned something. Hope you enjoy it. And, you know, the idea is to have this coming out every two weeks, so talk to you again in two weeks. Thank you.